Vanguard QLAC and Fidelity QLAC

Fidelity Investments and Vanguard Mutual Funds have made a name for themselves in the low cost investment field. Their low trading costs and low mutual fund management fees have brought billions of assets under management to both companies in the past three decades. In 2015 both companies added income annuities to sell to their existing client base including the deferred income annuity also know as a longevity annuity or QLAC. And on July 2nd 2014 the US Treasury Department made law in the Federal Registry a QLAC (Qualifying Longevity Annuity Contract). This “qualified” longevity annuity was now tax favored. The main benefit of the QLAC is to allow IRA owners the ability to delay the required minimum distribution (RMD) requirement to past age 72 and not have to pay taxes on that distribution until up to maximum age 85 if selected. The Federal government realized that longevity and outliving your assets would be a strain on Social Security system as people live longer lives. The QLAC incentive of tax deferral until income start , latest age 85, and automatic guaranteed income payments could release the stress on social security.

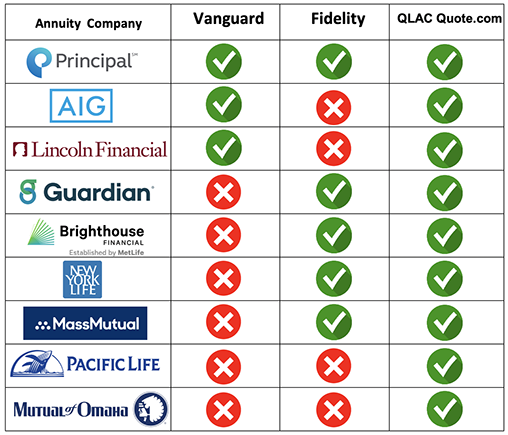

But where is the QLAC option at Fidelity and Vanguard? Nowhere to be seen? Remember annuities such as the QLAC can only per underwritten by an insurance company. Only an insurance/ annuity carrier can guarantee lifetime income like the Qualifying Longevity Annuity Contract does. As of 2016 both investing companies, Vanguard and Fidelity, offer annuity purchasing services outsourced to a third party insurance agency companies. Vanguard contracts QLACs from 3 providers out of 10. Fidelity has little more insurance providers with 4 out of ten companies. Both Vanguard and Fidelity being insurance agencies regulated by their home state, they receive commission directly from the insurance annuity QLAC companies they offer; Vanguard even charges you one time 2% on the purchase deposit amount which is reflected in now a lower income payment to the annuitant. An example of $100,000 purchase of a longevity annuity at Vanguard would cost you a fee of $2,000!

See Vanguards disclosures

" Vanguard Annuity Access is provided by Vanguard Marketing Corporation, d/b/a VMC Insurance Services in California. Fixed annuities purchased through Vanguard Annuity Access are subject to a one-time transaction fee. The fee is equal to 2% of the purchase amount."

Vanguard or third party potentially also receives commission less than 5% for the QLAC sale or some type of other compensation, however this was not disclosed. Fidelity doesn't use the 2% client fee directed to the QLAC annuity holder but uses the more traditional one time commission that is paid by the insurance company to the agent.

Fidelity offers the following QLAC insurance carriers: Guardian Life, Mass Mutual, Brighthouse, New York Life and Principal. Vanguard's QLAC offerings are limited to Lincoln Financial, Symetra Life and Principal.

To see the other six QLAC providers and for a no cost or no fee real time QLAC quote go to www.QLACQuote.com where we compare the top 5 QLAC approved companies to find you the best income amount. QLACQuote.com has digital applications and transfer forms online to speed your QLAC purchase. The IRA transfer to your new QLAC is a non taxable event and done thru a simple form that allows your QLAC provider to work with your IRA custodian directly with your approval.

Updated September 2019:

Vanguard has announced that they will stop providing access for their investors to annuities.

A larger provider of annuities in the prior decade, Vanguard has left the largest generational demographic baby boomer high and dry. Guaranteed income is a key part of retirees financial plan. Transamerica will administer the existing Vanguard variable annuities going forward. Income annuities including QLAC and SPIA or immediate annuities talked about above will cease going into December 2020.

“While insurance-based options can be an appropriate choice ..., annuity administration is not central to our long-term product and service plans. We’re deepening our focus on our core priorities delivering industry-leading funds and ETFs,” said Karin Risi, Managing Director of Vanguard’s Retail Investor Group.

Some details of the requirements to become a QLAC:

- Any 401k, Defined benefit, 457b, Pension Plan, 403b and all pre-tax IRAs, excluding Roth IRA, can be invested into a QLAC.

- The cumulative dollar amount invested into QLACs across all retirement accounts may NOT exceed $200,000 as of 2023.

- The QLAC must begin income payments at the latest by age 85.

- The $200,000 dollar amount will be indexed for inflation, CPI, adjusted in $10,000 increments. This $200,000 dollar amount was increased January 2023 from $125,000 limit established in 2014.

- The QLAC must provide fixed income payouts; COLA (cost-of-living adjustment) increases are an approved option.

- The QLAC can have an optional “return of deposit” death benefit option before the income start date and also have a return of deposit death benefit after income starts. Installment refunds or lump sum death benefits are the two options available.

By not having to take the required minimum distribution (RMD) every year after age 72 until age 85 gives the QLAC owner huge tax savings.

Get Your Quote in 1 Minute or Less!

<<<<<<<<<<<<<<

Give us one minute and we’ll give you an instant live QLAC annuity quote. It’s that easy. Then, if you like the rates (and we’re pretty sure you will), simply apply online along with your temporary locked in income rates.

The quote is free and there is no commitment. We don't sell your information or forward it onto a third party.

QLAC Qualifying Longevity Annuity Contract | Copyright 2012-2019 Income Quote LongevityInsurance.com